A year ago today, the markets were shaken by the relaxation of the Yen transport trade. While Japan moved to a stricter monetary policy and bond yields increased, the loan strategy in a low interest currency like Yen to buy higher yield assets has become less attractive.

At the time, capital quickly fled risk assets. Bitcoin (BTC) has dropped sharply, lowering almost 30% to $ 49,000, a level previously seen at the time of the US spot starts in January 2024.

Since then, however, the largest cryptocurrency by market capitalization has strongly rebounded, gathering more than 130% in the past year. Traditional markets have also worked well, S&P 500 increasing 24% and gold appreciating 40%, reflecting growing demand for risk and defensive assets.

On the other hand, the dollar index (Dxy), a gauge from the American currency against a basket of peers, has weakened at just under 100, against 103, long -term bond yields worked above. The 10 -year -old American yield increased to 4.2% against 3.7%, while 30 years increased to 4.8% against 4.0%. The quarters were amplified by international interest rate measures, climbing the United Kingdom at 30 years to 5.3% from 4.3% and the rowing in Japan more than 3% compared to 1.9%.

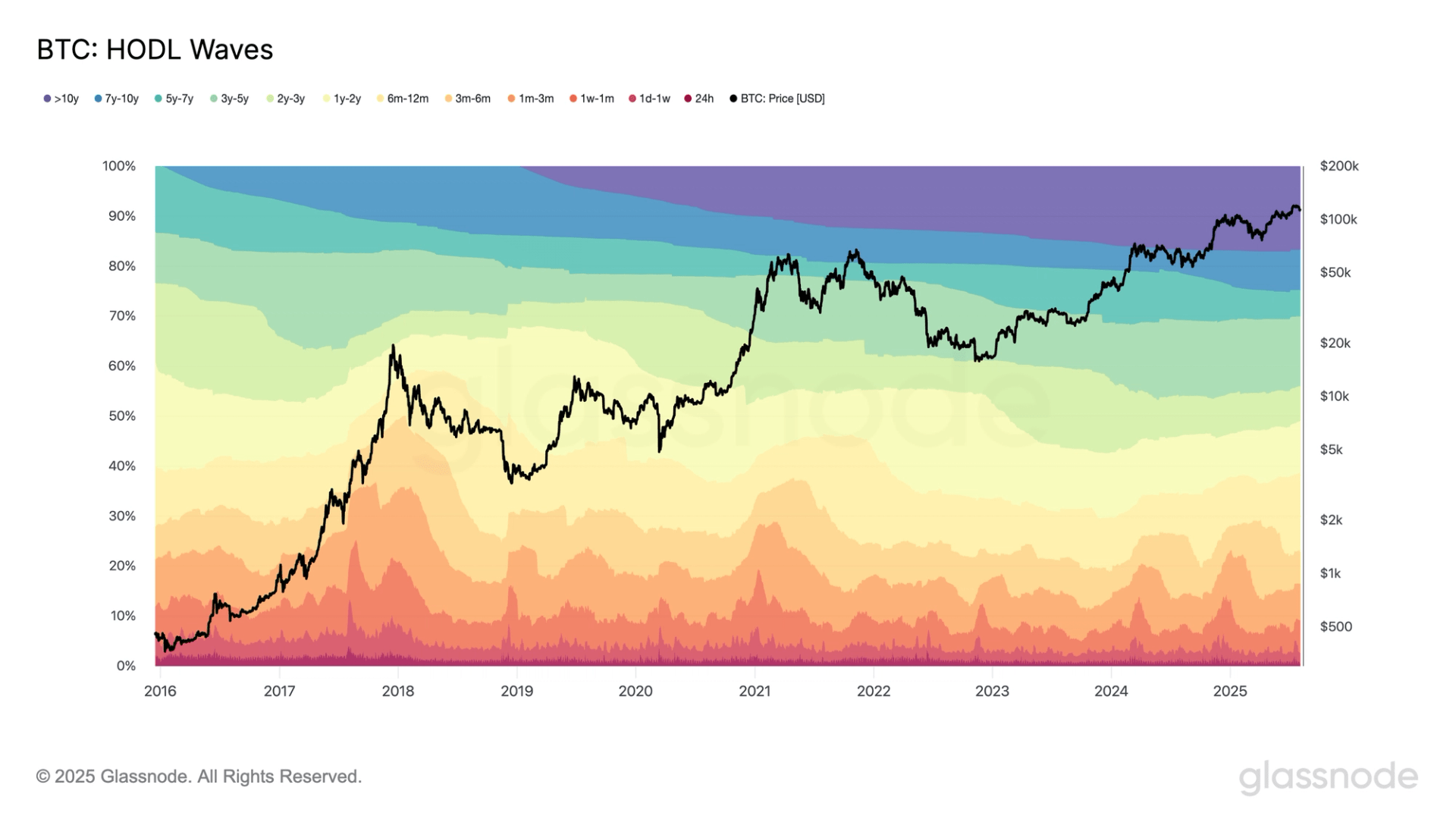

Despite price volatility, long -term bitcoin holders have regularly increased their share of the offer.

According to the Hodl Wave graph of Glassnode, which visualizes the distribution of the Bitcoin offer by age, each colored band represents the percentage of existing BTC which has grown for the last time in a specific time range. The groups show collectively since the duration of the parts, offering an overview of the behavior of investors and conviction over time.

The 7 to 10 -year cohort now holds more than 8%, against 4% a year ago, while holders of 6 to 12 months increased from 8% to 15%. This suggests that longer -term holders remain confident and still accumulate, while new investors have entered the market during the rally.

While a higher percentage of offers is now held by holders of less than 3 months than in 2024, which indicates that many buyers probably entered higher prices, possibly hunting the summits rather than buying the stockings.