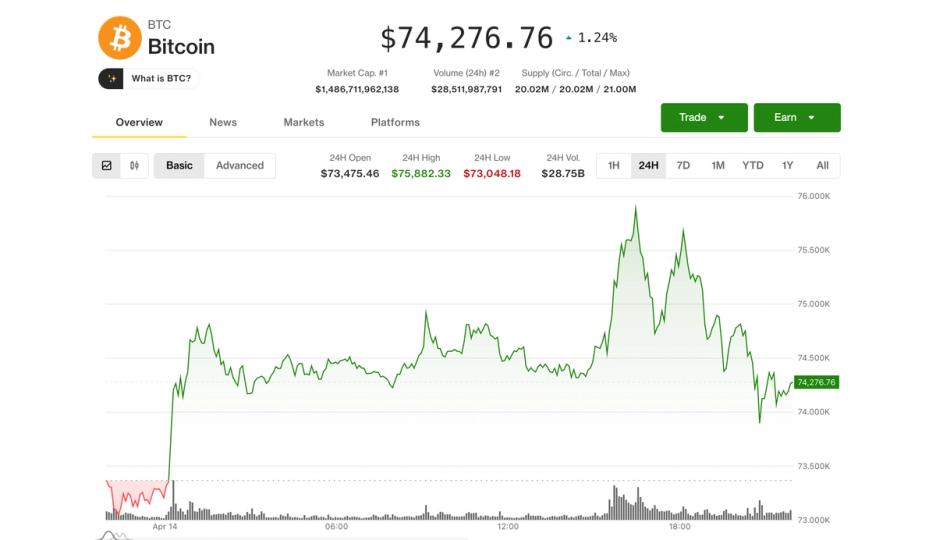

Bitcoin started the day with a promising breakout chance, but the rally stalled at a familiar brick wall that has kept prices in check for more than two months.

After briefly surpassing $76,000 – a key resistance level – the biggest crypto reverse price, falling below $74,000 later in the session. It still maintained a 1.3% gain over the past 24 hours, recently changing hands at nearly $74,300.

Ether (ETH) followed a similar path, falling over $2,400, but still outperformed, rising 2.5% daily.

Traditional markets saw no such reversal, with the Nasdaq closing at its session high, up 2%. The S&P 500 rose 1.2% and is now just a few points away from a new record high — a stark contrast to bitcoin, which remains about 40% below its all-time high of $126,000.

However, the conditions are ripe for a rise in cryptocurrencies, even if Tuesday’s breakout did not hold.

According to Vetle Lunde, head of research at K33 Research, funding rates for Binance Bitcoin perpetuals have remained negative for 11 consecutive periods despite the recent rally, indicating that traders are still bearish even as prices rise. At the same time, open interest has increased, suggesting new short positions are being added rather than closed, he said.

That combination has historically paved the way for strong gains, he said.

The 30-day average funding rate has now been negative for 46 consecutive days, Lunde added, matching the prolonged bearish positioning seen during periods of past market stress, such as after the FTX crash in late 2022 and the mid-2021 bear market when China banned bitcoin mining.

“Comparable risk aversion regimes have always been attractive entry points for BTC,” Lunde said, as crowded short trades were forced to unwind.